Last Thursday (September 17), the Federal Reserve left rates unchanged due to low inflation, recent turmoil in financial markets and in economies abroad, particularly China.

Markets were pricing less than 30% chance of rate-hike and most people in the financial markets were not expecting rate-hike. Well, not me. I was actually expecting 0.25%, 10 basis points rate increase, as I stated in my previous post.

“Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” Federal Open Market Committee (FOMC) said in statement. They are referring to events that took place in August, that can be described in one word; uncertainty.

Before we go any further, let’s compare the last two Fed statements.

Statement Comparison in PDF

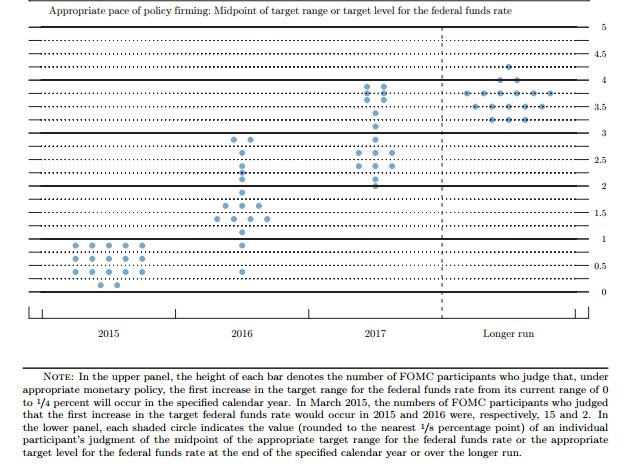

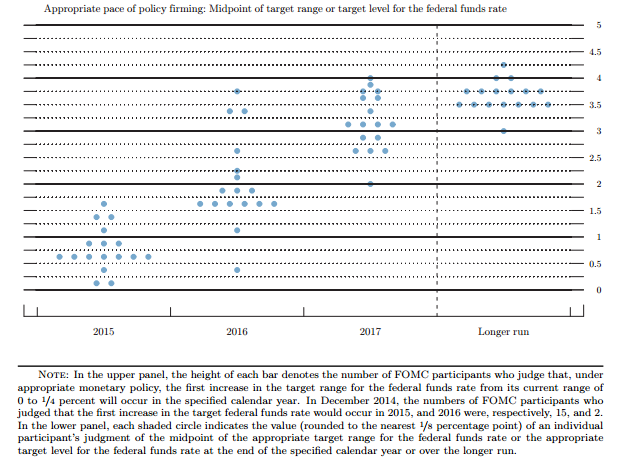

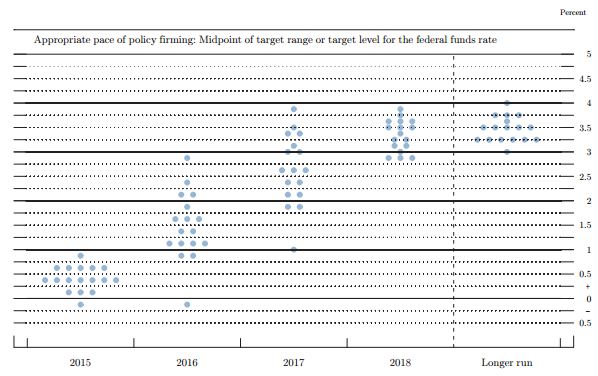

According to the Fed’s famous “Dot Plot” – that is where committee members think interest rates are going – one committee member, for the first time ever, thinks the U.S needs to move to negative interest rates until the end of 2016.

During the press conference, Janet Yellen – the chairwoman of the Fed – indicated that negative rates were not “seriously considered at all today” and that the policymaker in question was “concerned by the inflation outlook”. The Fed looks at a model “Phillips Curve” which states that inflation and unemployment have a stable and inverse relationship. It hasn’t been working lately.

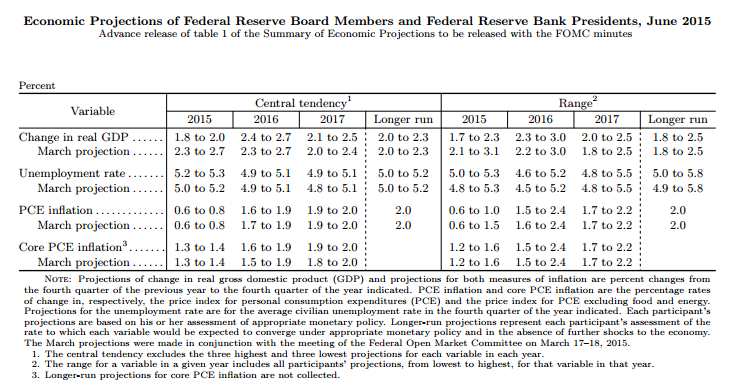

We know, as of today, both employment and inflation is low, likely due to the fact that many people are not in labor force and they are not included in unemployment calculation and due to low energy prices.

She said something that I found very interesting, “That’s something we’ve seen in several European countries. It’s not something we talked about today. Look. If not– I don’t expect that we’re going to be in the path of providing additional accommodation but if the outlook were to change in a way that most of my colleagues and I do not expect and we found ourselves with a weak economy that needed additional stimulus, we would look at all of our available tools and that would be something that we would evaluate in that kind of context.” This shows that even the Fed is uncertain about the future and another quantitative easing is a possibility.

If you want to see the body language from Yellen as she said it, go watch the press conference video. It can be very interesting. Any body language experts here?

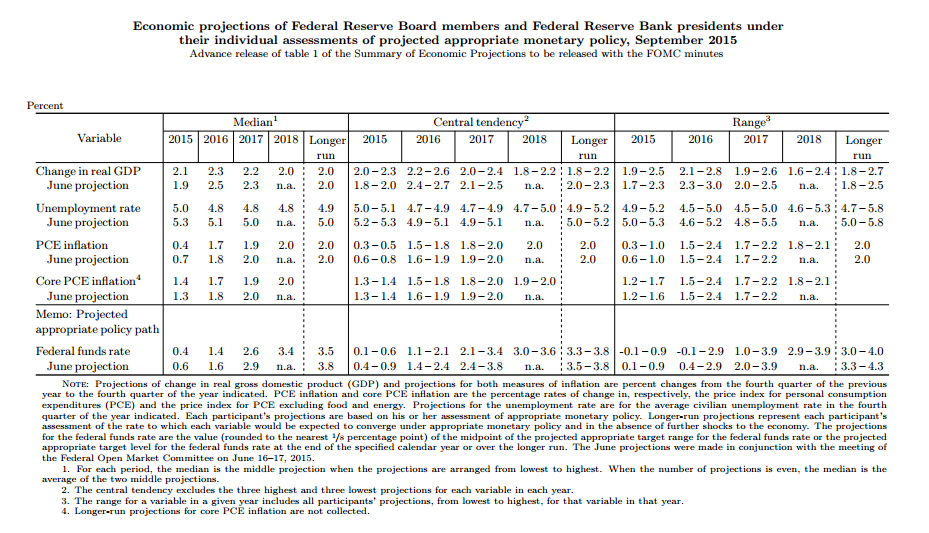

The Fed also raised growth forecast for the year and cut unemployment projection.

Yellen expressed that some countries other than China are also danger to the U.S, “…we saw a very substantial downward pressure on oil prices and commodity markets…significant impact on many emerging market economies that are important producers of commodities, as well as more advanced countries including Canada, which is an important trading partner of ours that has been negatively affected by declining commodity prices, declining energy prices….important emerging markets have been negatively affected by those developments. And we’ve seen significant outflows of capital from those countries, pressures on their exchange rates and concerns about their performance going forward. So, a lot of our focus has been on risks around China but not just China, emerging markets, more generally in how they may spill over to the United States.”

Back to “wait and see” mode again. Weak start in the year hammered the chances of rate-hike in June. Now, outsiders hammered the chances of rate-hike in September. Next stop?

If the current situation stays unchanged, I expect rate increase of 0.10% (again) in October (FOMC press conference will be called if the Fed decides to change rates). But, the current situation might get much worse. The bad news might come from China again.

Xi Jinping, China’s president and Communist Party chief, will arrive in the U.S next week to meet President Obama and business leaders. After the meeting when Mr. Xi is back in China, unpredictability arrives.

China would not want to create tension with the U.S before they meet face-to-face. Thus, unpredictability comes in two or three weeks. China might devalue their currency again, by 5% or more. They might even dump much more U.S Treasuries again.

It’s reported that China dumped U.S Treasurys of $83 billion and $94 billion in the month of July and August, respectively. Why would China sell U.S Treasurys? China is in dire need of cash. Capital outflows are increasing substantially and their stock market are declining substantially. China would want to cut its holdings of treasurys to support the yuan.

According to latest data from the U.S Treasury Department, China’s holdings of U.S Treasuries was $1.240 trillion in the end of July (is probably much less now), the smallest since February 2015. In end-June, China held $1.271 trillion. China remains the world’s largest holder of U.S debt. What does that mean for the U.S?

If U.S’s #1 lender stops supporting or stops buying U.S debt, the cost of everything that depends on Treasury rates could rise, putting pressure on the Federal Reserve and prevent the Fed from raising rates. Treasury yields (inverse relationship with prices) are the benchmark that sets the cost of borrowing.

China’s abandonment of U.S Treasury debt is a warning.

Imagine if China’s major trading partner, Japan, joins China in selling U.S Treasuries. Japan is the second-largest holder of U.S. Treasuries, with $1.197 trillion in July. The devaluation of Yuan will make Japanese exports less competitive. Japan’s economy is still suffering despite Abenomics. As I stated in my post “Global Markets Crash + Asian Crisis Part 2“, Abenomics has failed. Soon enough, Japan might also be in dire need of cash and they might start cutting their holdings of U.S Treasuries.

Recently, Standard & Poor’s slashed its ratings on Japanese debt from AA- to A+ because of weak economic growth, blaming Abenomics “…we believe that the government’s economic revival strategy–dubbed “Abenomics”–will not be able to reverse this deterioration in the next two to three years.” According to Standard & Poor, Japan’s Debt/GDP ratio currently stands at 242.4%, a dangerous level for developed country.

I believe Bank of Japan (BoJ) will increase its purchases of government debt to cover the danger of Japan’s Debt/GDP ratio and will sell portion of U.S Treasurys.

We can conclude everything will probably get much worse. The Fed will have no other choice, but to start another round of quantitative easing. In other words, debt monetization, a process of buying Treasury and corporate debt on the open market, increasing money supply. When increasing money supply, interest rates should fall.

The Fed is being held hostage by outsiders, such as China and Brazil. It probably won’t end well for the U.S, promoting another round of Quantitative Easing.

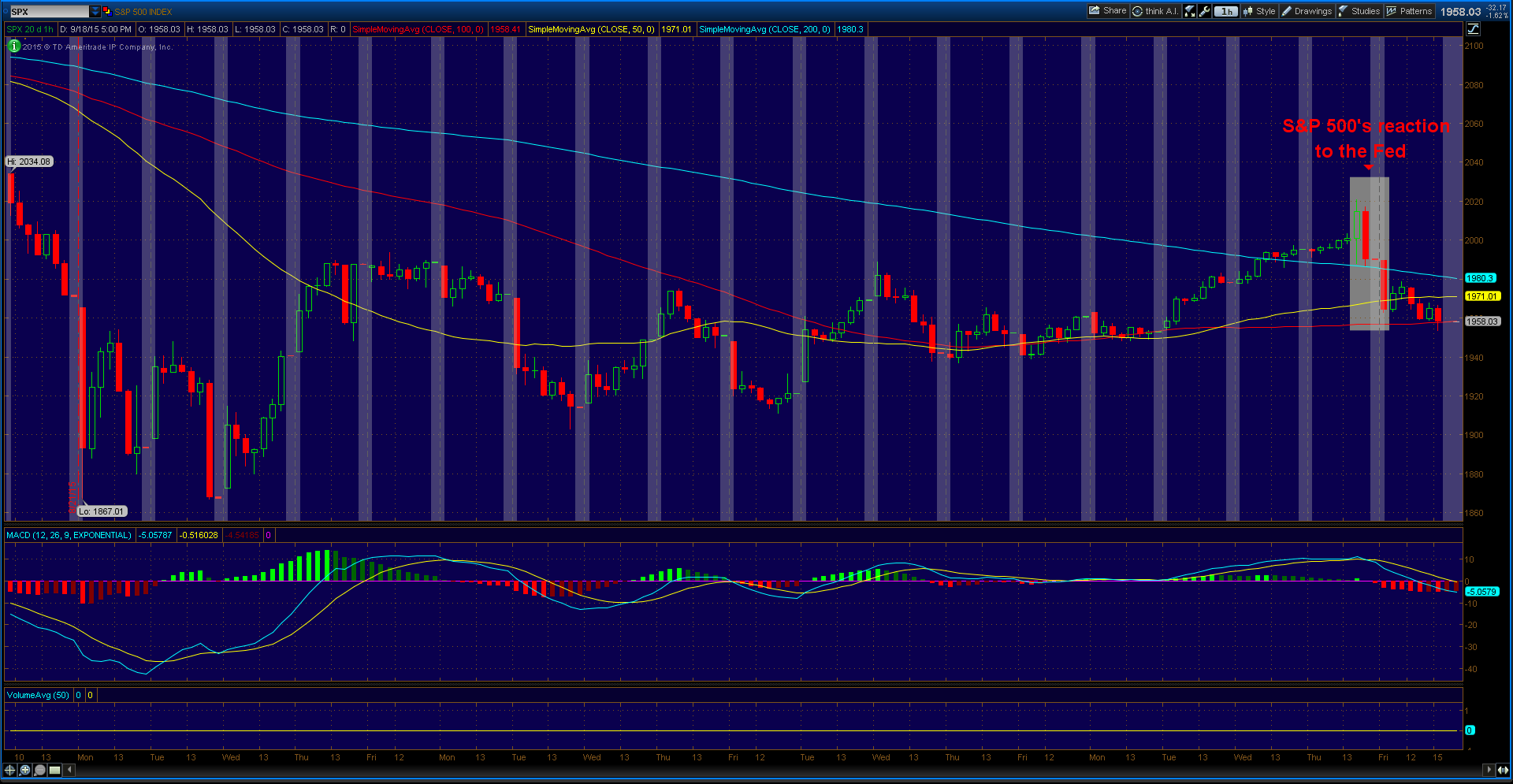

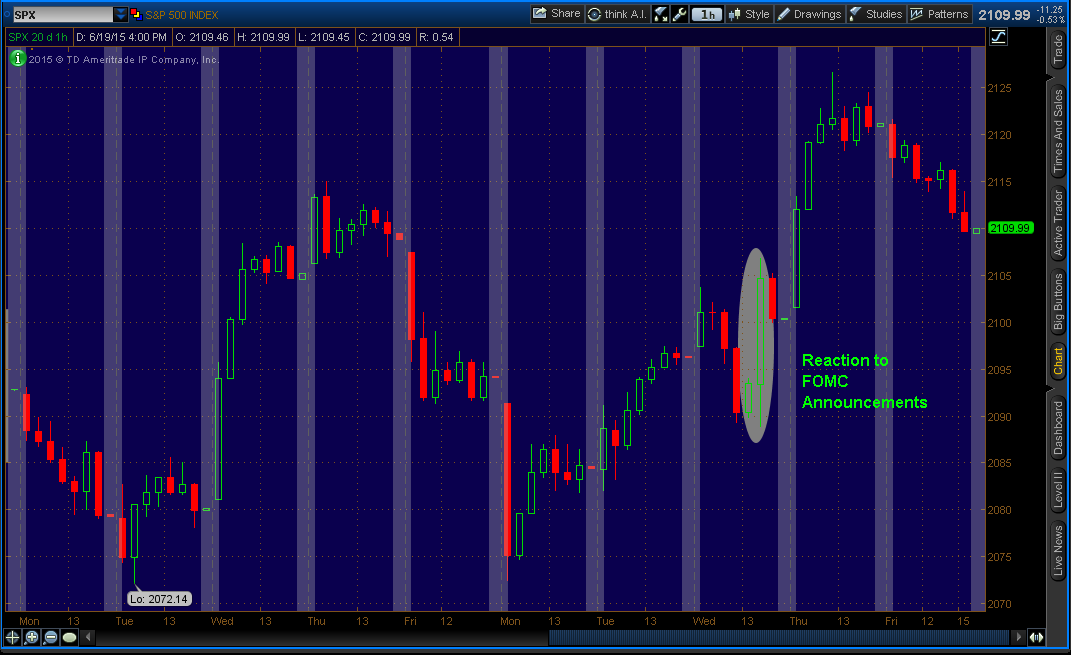

Markets’ reactions to the Fed report: