In this post, I will be giving an update on the investment ideas I wrote about.

Note: “Average price” includes Dividend Reinvestment Plan (DRIP) – the dividends I received were used to buy additional shares in the company.

On February 16, 2015, I wrote about Microsoft (NASDAQ: MSFT) and believed it was a strong buy. Ever since then, MSFT is up 19.07%, from $43.95 to $52.33 (dividends not calculated). On December 29, 2015, MSFT reached $56.85, the highest since 2000. I do not own the shares of MSFT. Yes, I did miss the opportunity. At the time, I couldn’t afford it to buy enough shares and cover the commission fees.

Microsoft Corporation (MSFT) – Daily

On April 12, 2015, I wrote about General Electric (NYSE: GE) and believed GE was also a strong buy (it still is). Ever since then, GE is up only 1.39%, from $28.06 to $28.45 (dividends not calculated). On December 28, 2015, GE reached $31.49, the highest since May 2008. I do own the shares of GE. I bought it in August 2014. The average price I own at is $25.87. I’m currently up 9.97%.

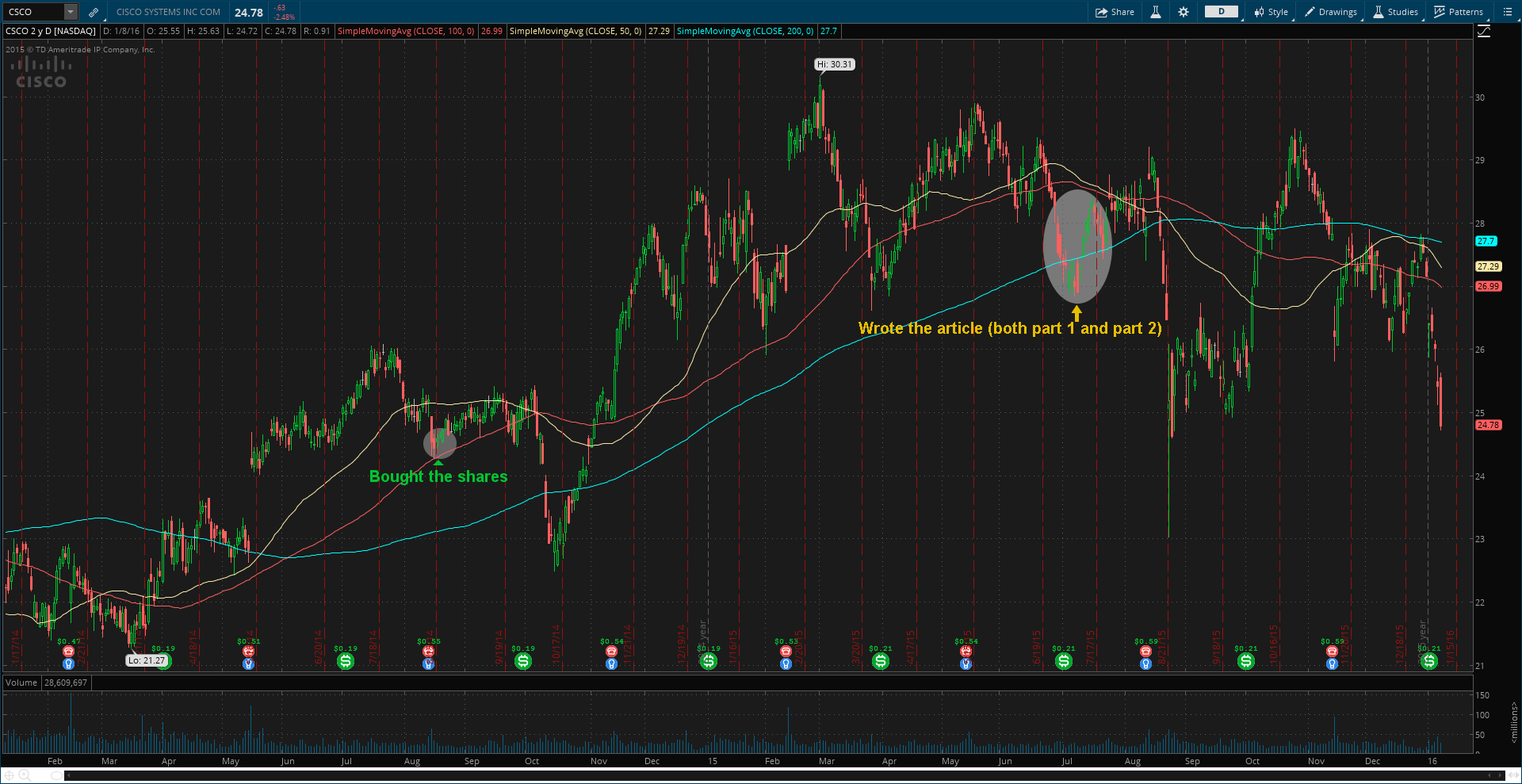

Cisco Systems, Inc. (CSCO) – Daily

Last summer, I wrote about Cisco Systems (NASDAQ: CSCO) (article part 1 and part 2) and believed it was undervalued (it still is). Ever since then, CSCO is down 11.47%, from $27.99 to $24.78 (dividends not calculated). I do own the shares of CSCO. I bought it in August 2014. The average price I own at is $24.73. I’m currently up mere 0.2%. I will take advantage (buy more shares) of lower prices.

Cisco Systems, Inc. (CSCO) – Daily

On November 21, 2015, I wrote about Eli Lilly (NYSE: LLY) and believed it was overvalued (it still is). Since then, LLY is down 3.85% from $85.50 to $81.25 (dividends not calculated). I’m not short on LLY. I cannot afford to short it, due to my capital.

Eli Lilly and Company (LLY) – Daily

On December 26, 2015, I wrote about GoPro (NASDAQ: GPRO) and believed it is a buy (it still is). Since then, GPRO is down 12.10% from $18.34 to $16.12.

Ahh! GoPro (NASDAQ: GPRO). A stock that gravity took over. It crushed from $98.47 (early October 2014) all the way down to $15.90 (mid December 2015). Boy, was Citron Research right, when they predicted share-price would drop to $30 within a year, in November of the last year.

And what now? Is this end of GoPro or is there more?

As for me, I’m very skeptical of the market. I’m someone who loves to go against the investments of the crowd.

For example, when the Alibaba (NYSE: BABA) was launched, I was convinced that the market was hyped about it and I didn’t find any intrinsic value in BABA’s share price. Recent market sentiment about GoPro is SELL SELL SELL!!! Me being the skeptic, I say BUY BUY BUY!!!

And it’s not just because of my skepticism of the market, but because of Karma and more.

Karma is coming in 2016 for the short-sellers of GPRO. So take your profit while you can. GoPro has planned to launch its first drone, Karma in 2016. The introduction of a drone will expand camera maker’s product line, beyond making action cameras.

GoPro founder and CEO Nick Woodman said at the TechCrunch conference in September that the company is planning to launch a drone in the first half of 2016, “development is on track for the first half of 2016. We have some differentiations that are right in the GoPro alley.” Karma is finally coming.

Hollywood is eager to change the way they take aerial shots. Not long ago, they used helicopters (some still do) to shoot from bird’s point-of-view and it costs a lot. Drone makes it all cheaper. Not only cheaper, but also safer and opens more creative ways of shooting a video. In other words, drones can do what helicopters cannot do.

On May 28, GoPro announced at Google’s I/O conference that it will build a 360-degree camera array for stereoscopic spherical videos. With the help of Google Jump, Google’s virtual reality system, GoPro’s camera array, Odyssey can make videos like this. I believe the Odyssey can be very useful for real estate market. “360-Degree Real Estate Tour – Brought to you by GoPro.”

Oh, did I mention Odyssey has 16 cameras that work together as one? I repeat, 16. Hey GoPro, why don’t you knock out your useless and wasteful $300 million buyback program out of the park? According to its third-quarter SEC filing (10-Q), GoPro stated,

“To the extent that current and anticipated future sources of liquidity are insufficient to fund our future business activities and requirements, we may be required to seek additional equity or debt financing. In the event additional financing is required from outside sources, we may not be able to raise it on terms acceptable to us or at all.”

They spend 345x more on buybacks than they do on research and development. So GoPro, eliminate your worthless buyback program. “Customize” the money into research and development, and acquisitions. Customize the Odyssey. 16 cameras? Really? Reduce the size and improve the quality.

I strongly believe GoPro should acquire a small thermal imaging company. Thermal imaging can be a perfect fit for drones. I suggest GoPro acquires Seek Thermal, designer and manufacturer of high quality thermal imaging products. If GoPro acquires Seek Thermal or a different thermal imaging tech company, they will be able to reach sectors such as firefighting and agriculture. Diversified!

Another great acquisition can be Vuzix (NASDAQ: VUZI), a Google Glass rival, and a leading developer and supplier of smart glasses and video eyewear products in the consumer enterprise and industrial markets. Vuzix holds over 41 patents and 10 additional patents pending. Market cap. is currently $104.39 million. With $513 million cash on hand, GoPro can afford the acquisition. In January, Vuzix received a $24.8 million investment from Intel (NASDAQ: INTC). Intel bought preferred stock that is convertible into common shares equivalent to 30% of Vuzix.

In the third-quarter, GoPro’s revenue increased 43% year-over-year (Y/Y) to $400.3 million. On non-GAAP basis, its net income, operating income, and operating expenses increased 103.9% Y/Y, 71.7% Y/Y, and 44.3% Y/Y, respectively. On GAAP basis, it increased 28.58%, 105.36%, and 43.78%, respectively. The growth isn’t bad for a company with a market cap. of $2.49 billion. However, its inventory days increased 80.6% Y/Y from 67.7 to 122.3.

There are buyout rumors and one of the potential suitors being Apple (NASDAQ: AAPL). While this is a great news, it is not likely to happen in the first half of 2016. I believe the management of GoPro would not want to sell the company until they see the outcome of Karma. If the outcome is positive, the company will not be sold next year. If it is negative, the company will be sold unless they have something up in their sleeves. Management’s actions should a sign of what’s to come.

I’m confident the founder of GoPro will turn things around next year. GoPro can be a leader in its field if it eliminates the buyback program and invests into the future. According to Futuresource Consulting, the global action camera market grew by 44% Y/Y in 2014. It is expected to grow at a compound annual growth rate (CAGR) of 22.2% between 2014 and 2019. GoPro should target not only sport enthusiasts, but the film and television industry, real estate, and other sectors such as, firefighting and agriculture. In order to do that, GoPro should first create a product that suits the sector’s needs. First impressions are important.

Disclosure: I’m currently long on the stock, GPRO, at this time (December 26, 2015).

Note: All information I used here such as revenue, net income, etc are found from GoPro’s official investor relations site and its SEC filings.

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.

On October 22, Eli Lilly (LLY) reported an increase in the third-quarter profit, as sales in its animal health segment and new drug launches offset the effect of unfavorable foreign exchange rates and patent expirations. Indianapolis-based drug maker posted a net income increase of 60% to $799.7 million, or to $0.75 per share, as its revenue increased 33% in animal health segment. In January 2015, Eli Lilly acquired Norvartis’s animal health unit for $5.29 billion in an all-cash transaction. The increase in the animal-health revenue helped offset sharp revenue decreases in osteoporosis treatment Evista and antidepressant Cymbalta, whose revenue fell 35% and 34% year-over-year, respectively. Eli Lilly lost U.S. patent protection for both drugs last year, causing patent cliffs. Lower price for the Evista reduced sales by about 2%.

Total revenue increased 2% to $4.96 billion even as currency headwinds, including strong U.S. dollar, shaved 8% off of the top line in revenue. Recently launched diabetes drug Trulicity and bladder-cancer treatment Cyramza helped increase profits, bringing a total of $270.6 billion in the third-quarter. Eli Lilly lifted its guidance for full-year 2015. They expect earnings per share in the range of $2.40 and $2.45, from prior guidance of $2.20 to $2.30.

Despite the stronger third-quarter financial results, I believe Eli Lilly is overvalued. Eli Lilly discovers, develops, manufactures, and sells pharmaceutical products for humans and animals worldwide. The drug maker recently stopped development of the cholesterol treatment evacetrapib because the drug wasn’t effective. Eli Lilly deployed a substantial amount of capital to fund Evacetrapib, which was in Phase 3 research, until they decided to pull the plug on it. The suspension to the development of Evacetrapib is expected to result in a fourth-quarter charge to research and development expense of up to $90 million pre-tax, or about $0.05 per share after-tax. Eli Lilly’s third-quarter operating expense declined 7% year-over-year, mainly due to spending on experimental drugs that failed in late-stage testing trials.

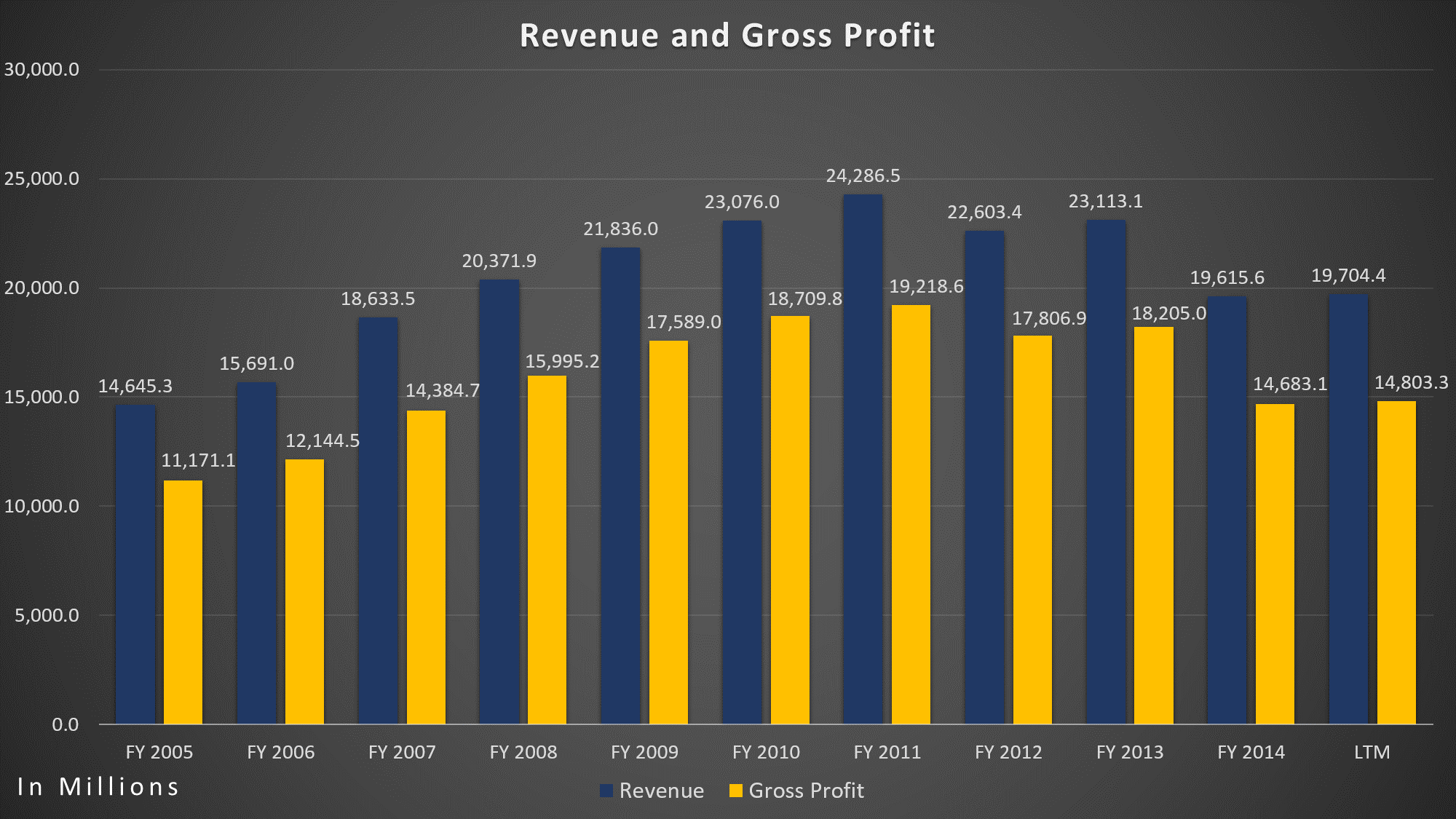

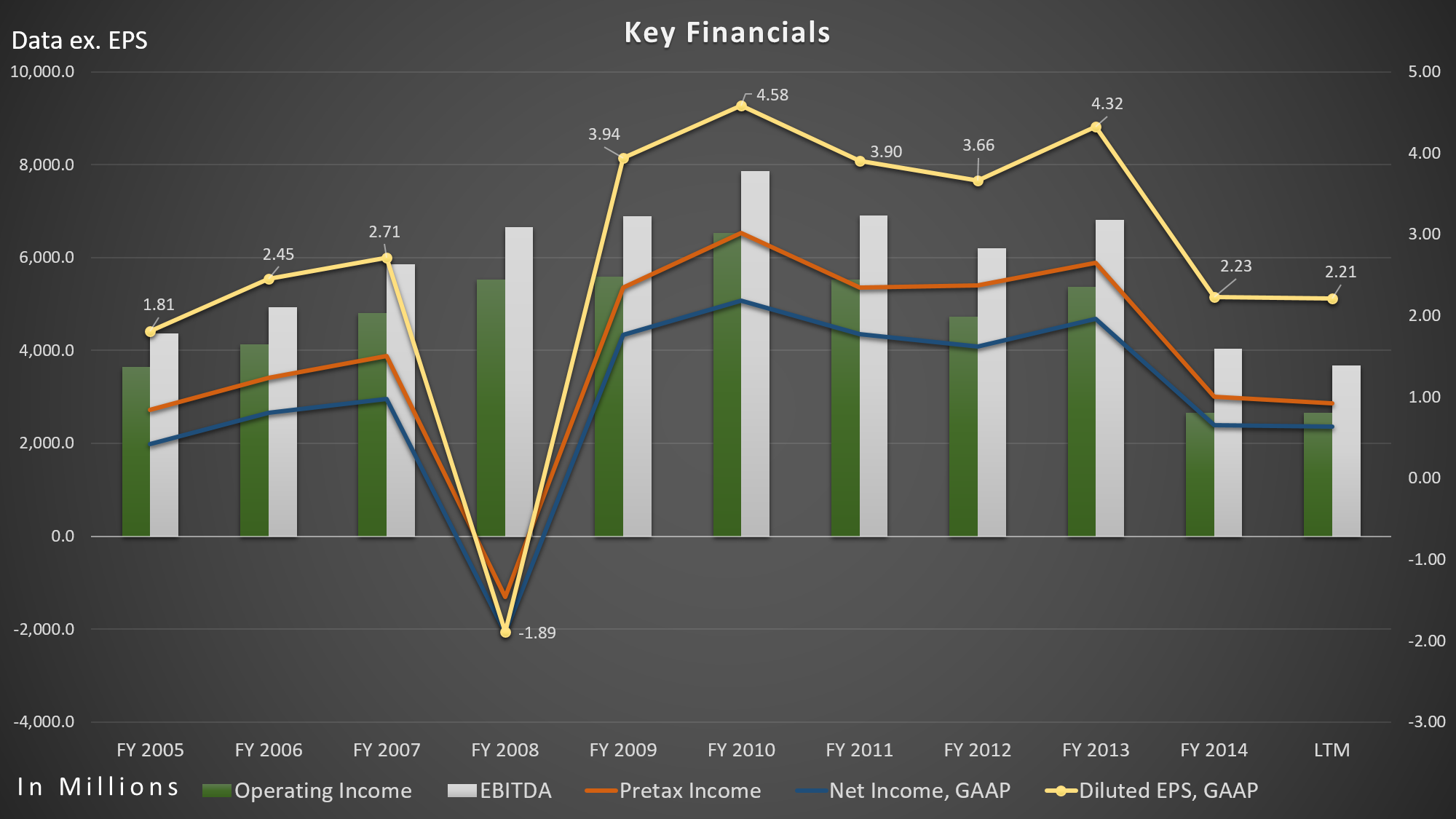

Eli Lilly’s market capitalization skyrocketed over the past five years by 122.76% to $90 billion, but their revenue, gross profit, net-income, operating income, as well as EBITDA, declined significantly. Over the past five years, its revenue decreased 14.61% from $23.08 billion to $19.70 billion (LTM), largely due to patent expirations. Gross profit and net-income declined 26.06% and 53.48%, respectively. Its operating income fell 59.18% over the past five years.

Eli Lilly – Revenue/Gross Profit

Eli Lilly – Key Financials

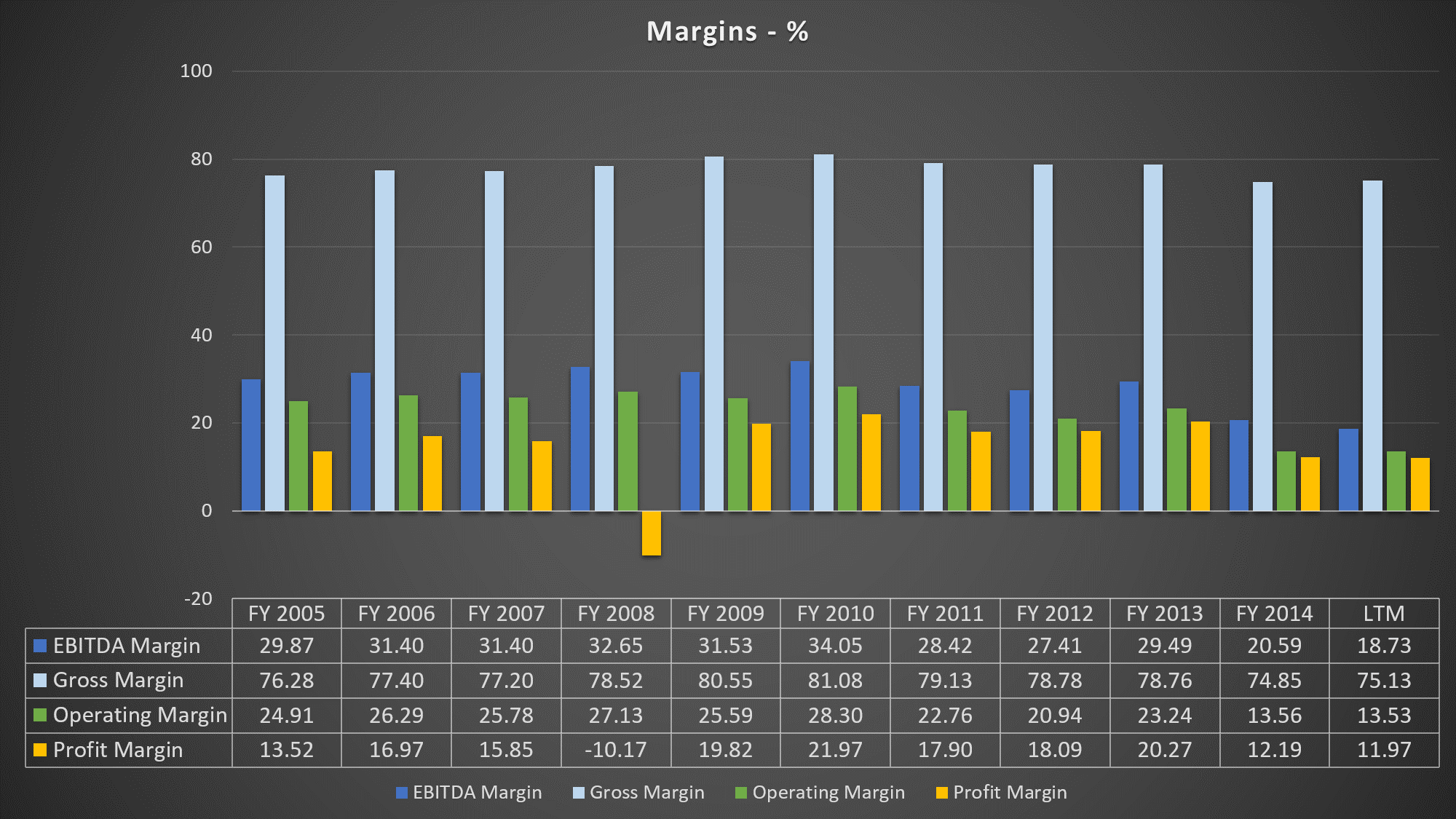

Its operating margin fell a halfway over the past five years from 28.30% to 13.53% (LTM). EBITDA margin, on the other hand, fell all the way to 18.73% (LTM) from 34.05%.

Eli Lilly – Key Margins

Meanwhile, shares of Eli Lilly gained 144.49% over the past five years. Its price-to-sales ratio too high compared to its history and to S&P 500. Its Price/Sales ratio currently stands at 4.6, vs. at 1.7 in 2010, while S&P 500 currently stays at 1.8 and industry average at 3.9. In addition to the falling revenue, gross profit, net-income, and EBITDA, its free cash flow fell significantly over the past five years by 72.24%, or fell 22.61% on a compounded annual basis.

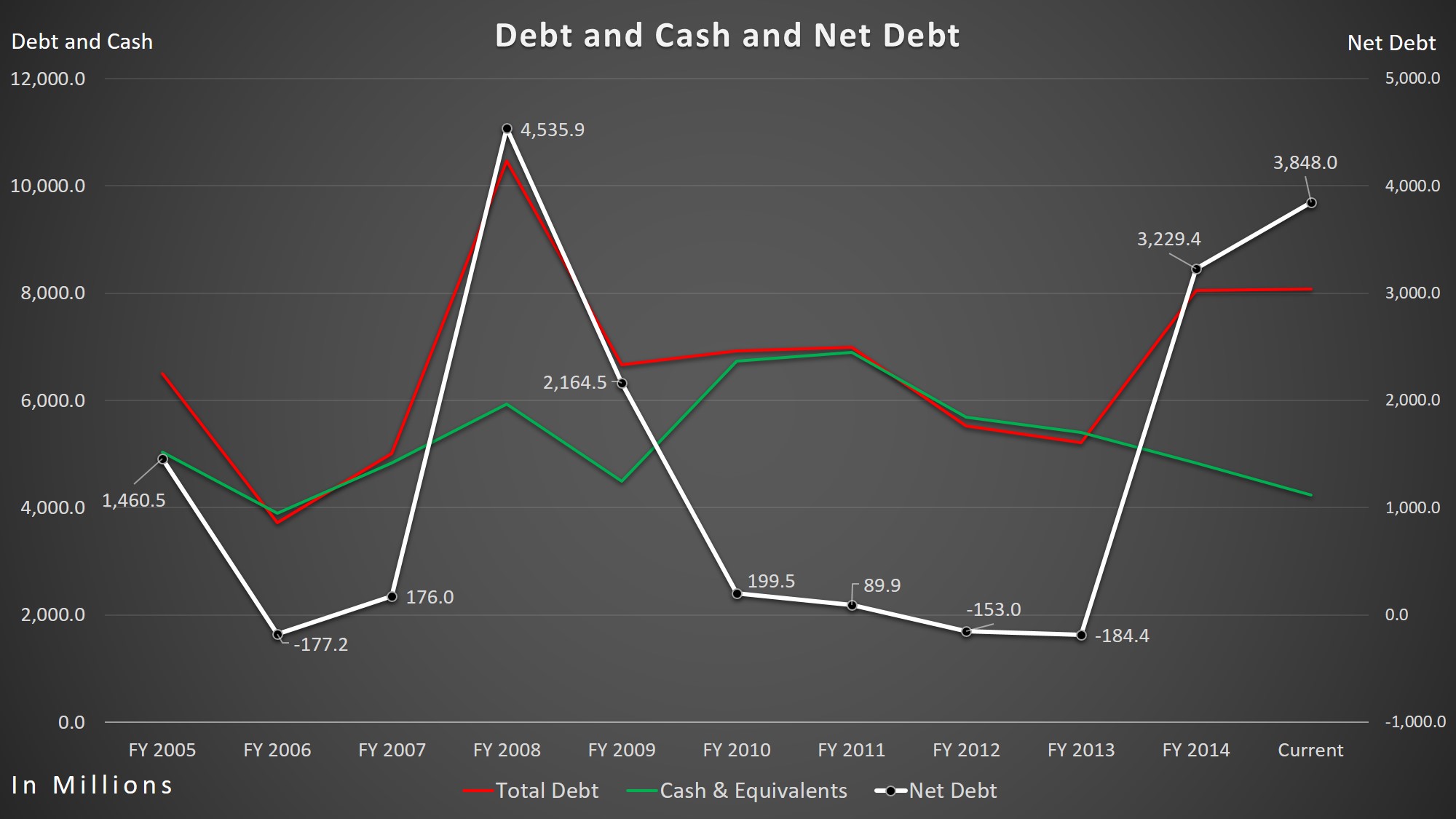

Not only did their cash flow fall, but their net-debt increased significantly. Its net-debt increased by a whopping 1789.87% over the past five years from $199.5 million to $3.85 billion. They now have almost twice as much of total debt than they do in cash and equivalents. I believe Eli Lilly is at a risk for poor future ratings by rating agencies, which will increase their borrowing costs.

Eli Lilly – Total Cash/Total Cash/Net-Debt

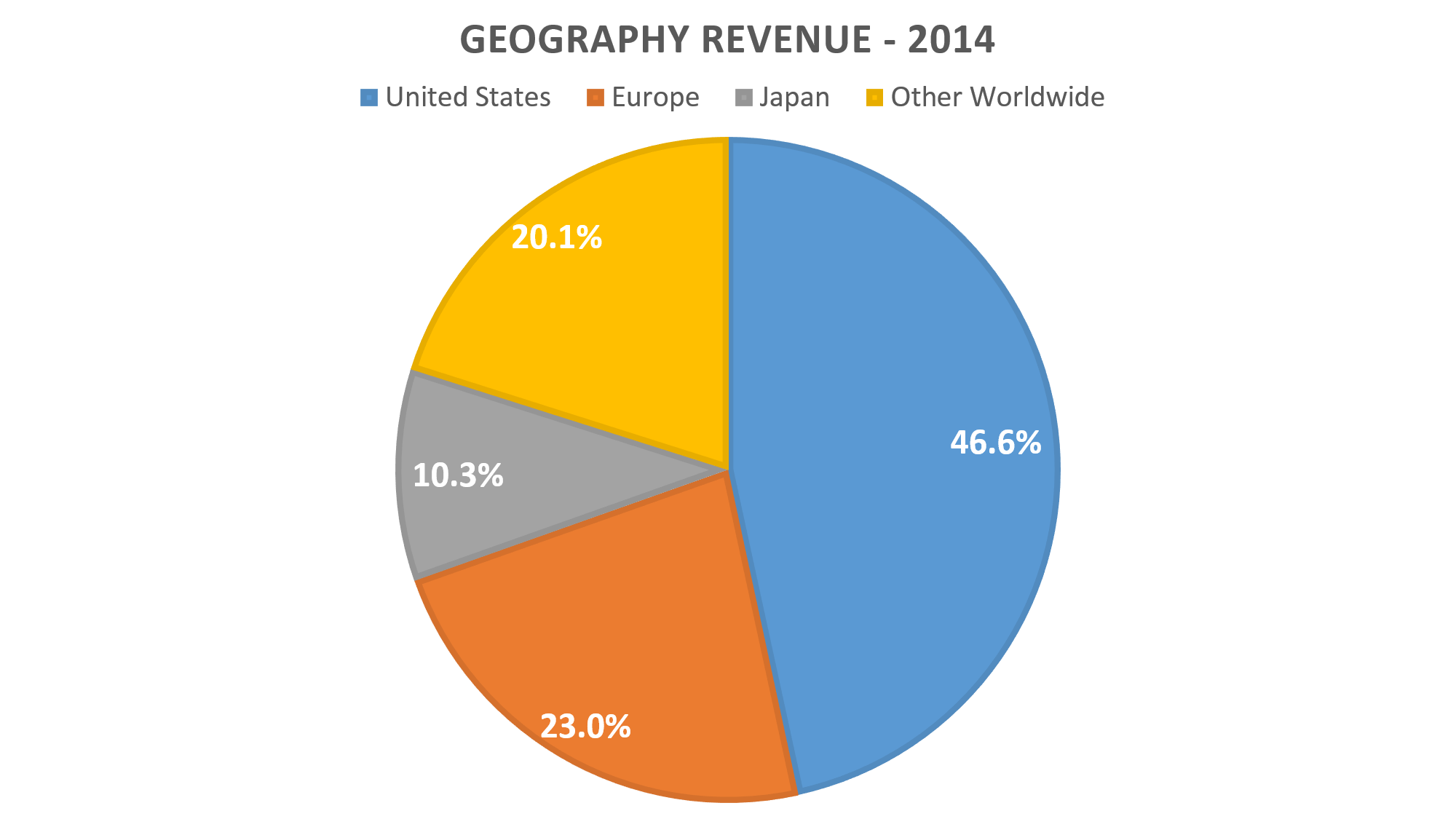

Strong U.S. dollar is an issue for Eli Lilly. Over the past five years, the dollar index increased 26.75%. Last quarter, its 49.2% of revenue came from foreign countries. Its revenue in the U.S. increased 14% to $2.54 billion, while revenue outside the U.S. decreased 9% to $2.42.

Eli Lilly – 2014 Geography Revenue

Eli Lilly’s dividend yield of 2.55% or 0.50 cents per share quarterly can be attractive, but it is undesirable. From 1995 through 2009 (expectation of 2003-2004), Eli Lilly raised its dividend. Payouts of $0.26 quarterly in 2000 almost doubled to $0.49 in 2009. Then, the company kept its dividend payment unchanged in 2010, the same year when its net-income, EBITDA and earnings per share (EPS) reached an all-time high. About four years later (December 2014), Eli Lilly increased the dividend to $0.50 quarterly. I still don’t see a reason to buy shares of Eli Lilly. The frozen divided before the recent increase was a signal that the management did not see earnings growing. With expected patent expiration of Cymbalta, their top selling drug in 2010, it is no wonder Eli Lilly’s key financials declined and dividends stayed the same. Cymbalta sales were $5.1 billion in 2013, the year its patent expired. In 2014, its sales shrank all the way down to $1.6 billion. Loss of exclusivity for Evista in March 2014 immensely reduced Eli Lilly’s revenue rapidly. Sales decreased to $420 million in 2014, followed by $1.1 billion in 2013. Pharmaceuticals industry continues to lose exclusivities, including Eli Lilly.

In December 2015, Eli Lilly will lose a patent exclusivity for antipsychotic drug Zyprexa in Japan and for lung cancer drug Alimta in European countries and Japan. Both of the drugs combined accounted for revenue of $866.4 million in the third-quarter, or 17.5% of the total revenue. They will also lose a patent protection for the erectile dysfunction drug Cialis in 2017, which accounted for $2.29 billion of sales in 2014, or 11.68% of the total revenue.

Besides the pressure from patent expirations, there is also regulatory pressures on drug pricing. According to second-quarter 10Q filing, Eli Lilly believes “State and federal health care proposals, including price controls, continue to be debated, and if implemented could negatively affect future consolidated results of operations.” During the third-quarter earnings call, CEO of Eli Lilly, John C. Lechleiter, said that price increases reflects many of medicines going generic and “deep discounts” government mandates for large purchasers.

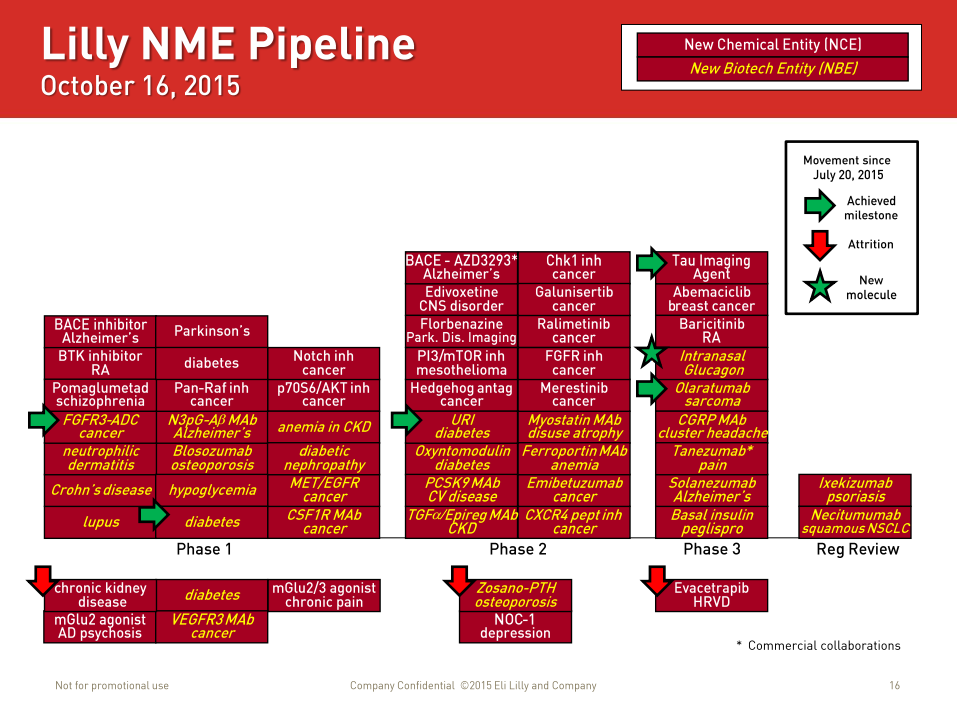

As of October 16, Eli Lilly had two drugs under regulatory review, nine drugs in Phase 3 testing, and 18 drugs in Phase 2 testing. Since the end of July, the drug maker terminated the development of few drugs, including evacetrapib in Phase 3, two drugs in Phase 2, and five in Phase 1. Out of total eight drug termination, only five drugs moved to the next stage of testing. I view the recent termination of evacetrapib as a major setback.

Compared to its peers, LLY’s Price-to-Earnings ratio is too high. Its P/E ratio (on GAAP basis) stands at 38.22 while industry average stands at 17.7. Four of its main peers, Pfizer (PFE), Johnson & Johnson (JNJ), Merck (MRK), and Sanofi (SNY) P/E ratio stands at 24.08, 19.63, 14.41, and 22.38, respectively.

Negative trends, tighter regulations, increasing competition and slowing growth makes Eli Lilly’s current valuation unjustified. I believe it will reach an average P/E ratio of its four main competitors, at 20.12, in the next three years. I expect EPS (GAAP) to contract. With current EPS of $2.21 (LTM, GAAP) and P/E ratio of 20.12, share price would be worth $44.46, down 47.37% from current share-price of $84.47. As EPS contracts, the share price of Eli Lilly will be much further down from $44.46 in the next three years.

Disclosure: I’m not currently short on the stock, LLY, at this time (October 21, 2015).

Note: All information I used here such as revenue, margins, EBITDA, etc are found from Eli Lilly and Company’s official investor relations site, Bloomberg terminal and morningstar. The pictures you see here are my own, except “Eli Lilly Pipeline – Third Quarter Earnings Presentation – Page 16”

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.